Friends, I hope you all have been well. I want to share a thesis on an asset that might surprise some of you.

It's Morpho, the token behind the second largest DeFi protocol by TVL. At first glance, you might be skeptical, which is understandable. The token has no value accrual at the moment and is in the middle of significant pending unlocks. My intent in this article isn't to shill this coin down your throats and tell you to buy, it's more so just to share a trend that I am incredibly bullish on, institutional defi, and how Morpho fits into that picture. Take everything I say with a grain of salt. Do your own work. Let's get into it.

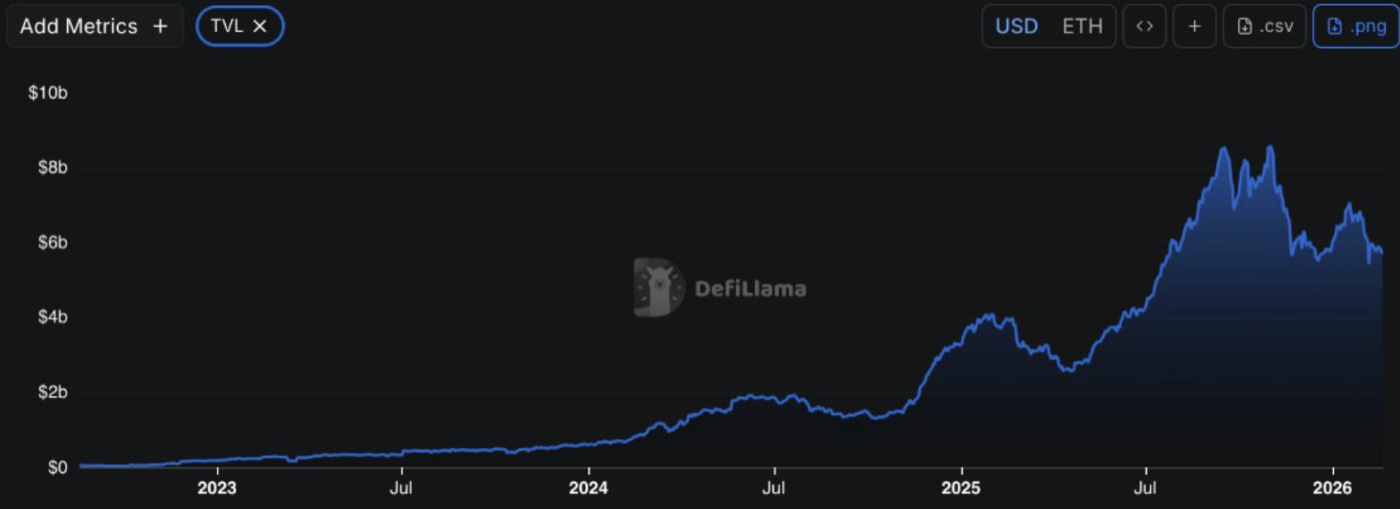

As of late February 2026, Morpho sits at a TVL just south of $6B, significantly trailing Aave at $27B TVL. But my thesis isn't fixated on the TVL, it's more so pertaining to Morpho's unique architecture, and how it differs from Aave.

In Aave-style pooled markets, all USDC suppliers sit in one USDC pool. Every USDC loan comes out of that same pool. The USDC suppliers are collectively exposed to the same set of borrowers who borrowed USDC against many different collateral types and risk profiles. While this is efficient, this creates an issue of shared risk profiling. For example, One USDC depositor might not want to be exposed to someone depositing USDE to borrow USDC, whereas they would be more comfortable with an ETH depositor borrowing, and vice versa.

Morpho differs from Aave in that lending exposure can be segmented into isolated markets/vault allocations, so you can have a vault that only lends USDC against, say, one collateral set and one LLTV/oracle/IRM configuration, instead of one monolithic USDC pool taking all borrowing profile risks. Morpho's infrastructure is permissionless, non-custodial, and immutable in nature. Every lending market is defined by five parameters: loan asset, collateral asset, liquidation LTV, oracle, and interest rate model.

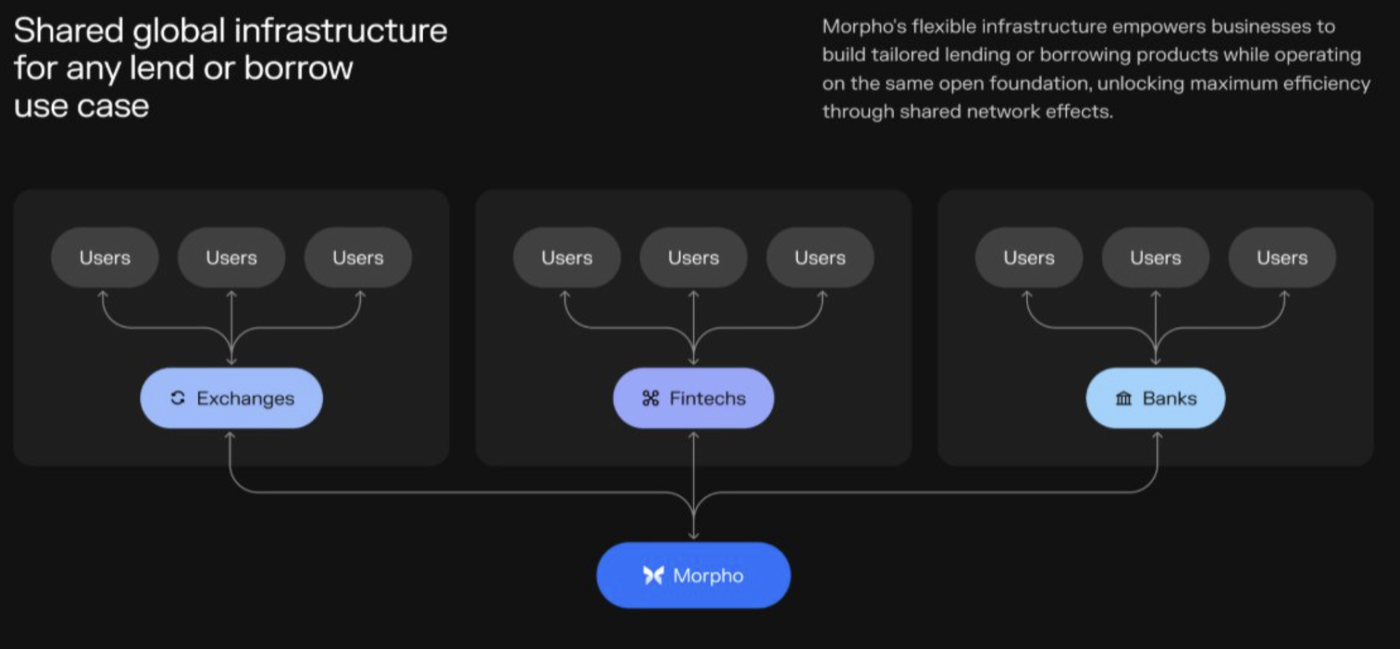

Monolithic pools are great and do serve a useful purpose, but it's not the correct solution for actors who have much more sensitive risk tolerance(s). Tradfi firms will not want to send client capital into publicly pooled risk systems with anonymous borrower environments and fixed risk parameters that were designed for retail. They want isolated, configurable, controllable credit environments. They want to white-label it. Slap their name on it. Tell their LPs they're "innovating in digital assets" while running Morpho infra under the hood.

From the outside, it'll look like "Apollo Credit Vault","BlackRock Treasury Vault", "Coinbase Institutional Lending Vault", "Robinhood Gold USDC Vault." But under the hood, all of these vaults will be operating on Morpho infrastructure. This is analogous to how institutions use AWS instead of building their own servers. Like how every startup runs on AWS but pretends they have proprietary infrastructure.

In January 2025, Coinbase launched BTC-backed loans for their users. These loans are provided by Morpho. One of the largest defi-cefi integrations I can think of in recent times. BTC holders on Coinbase can now leverage Morpho's stack to access deep USDC liquidity. As of now, there is around $1.15B in collateral posted and $631M in borrows through that integration alone.

Then there's Apollo. Back in Q1 2025, Apollo Global Management, which boasts nearly a trillion in AUM, collaborated with Securitize to tokenize their fund Apollo Diversified Credit Securitize Fund (aka ACRED). They also built a vault on Morpho that facilitates deposits of the ACRED token as collateral, and allows for USDC borrowing against it. This is just to provide access to leveraged yield farming, with Gauntlet's risk engine monitoring the risk buildup. For additional context, ACRED delivered a 9.41% return during its first year.

But Apollo's venture into onchain defi goes deeper than just through ACRED.

On February 14th, 2026, Morpho announced that Apollo affiliates would acquire up to 90 million MORPHO tokens (9% of total supply) over 48 months. Purchases would be facilitated via open market or OTC.

What I found interesting about this announcement is the reference to "ownership caps and transfer restrictions". It implies to me that this isn't some type of short term flip. To give backdrop, a large chunk of Apollo's AUM is in private credit. Morpho vaults are basically private credit infrastructure but put onchain. So it seems to me that Apollo is looking to own governance as a way to gain influence over the infrastructure that they intend to use more in the future. It's akin to a private credit firm acquiring equity in a clearinghouse. The only difference is that the equity is a token in this case. But the token isn't just a financial asset but also a right of influence and sway over the core infrastructure.

Real world assets are getting tokenized. Treasuries. Private credit. Real estate. Money market funds. All of it. And once they've tokenized onchain, what happens? They get hyperfinancialized on defi rails. That's what crypto does to everything. Actors will naturally want to borrow against these assets, to either free up liquidity or enhance yield strategies through looping strategies.

And where does that activity flow? Through lending infrastructure.

Credit is the largest financial market in the world. Global credit markets are already past $300 trillion. Private credit alone is $1.5 trillion and growing rapidly. Even if just a sliver migrates onchain, Morpho becomes essential A1 infrastructure for those newly minted assets.

Also another small detail, Morpho has heavily centered itself on Base, Coinbase's L2. Base has low fees, fast execution, and institutional credibility with direct integration into the Coinbase ecosystem. Institutions tend to follow the path paved by earlier institutions, and Base is positioning itself as the "compliant" chain. And Morpho (through Coinbase and Base) seems uniquely positioned to benefit from this.

Now, this is the most important part and the part that we know least about.

Currently, Morpho captures zero protocol level fees. This is intentional, they're doing what any firm would do, maximizing adoption before extracting value. But there's also a fee switch embedded in the smart contract. Once governance decides to, extracted value would flow freely to the token DAO. Morpho, with its vault architecture, could implement fees at multiple layers: vault management fees, borrow spread fees, protocol routing fees.

Let's assume a base case scenario of $10B TVL, 5% average borrow rate, and 80% utilization.

That's $8B in borrows generating $400M in annual interest. A 10% fee nets $40M, 15% is $60M, 25% is $100M. Let's apply a 20-50x revenue model to value the token.

Side note, I picked 50x as the upperbound valuation because (a) it's crypto (b) half of us don't even know what a valuation model is (c) it looked provocative when i typed it out

$40M revenue at 30x = $1.8B valuation. $100M revenue at 30x = $3B valuation.

This is before continued growth. If TVL hits $20B, these numbers double.

Apollo's incentive is clear. At 9% ownership, they capture 9% of any value created by fee activation. At $60M annual revenue and 30x multiple, that's $162M in value to Apollo.

Not going to sugarcoat it, there is a significant overhang on Morpho's token. As of now, only 55% of the total supply is circulating. There aren't really any massive cliff unlocks that you can wait to pass. It's something that I'd argue is worse: steady linear unlocks. Death by a thousand cuts. It's possible Apollo could become the de facto OTC bid for vesting supply, but this is only speculation.

At $1.40, MORPHO is pricing a $1.4B FDV. That's uncomfortably close to Aave when you also account for the fact that Aave has a much larger, more battle-tested TVL base. It's obvious that Morpho is being valued on future positioning, though the growth of curator managed vaults and white-label credit rails rather than current fundamentals.

If the protocol never activates fee capture, MORPHO remains a governance premium with no hard link between protocol activity and token value. This makes it quite difficult to justify a FDV of this size with 55% circulating and multi-year supply overhang.

The cleanest path to escape velocity is turning the fee switch on. Once Morpho starts taking a defined cut of borrower interest, you can do some pretty silly moon math to value the token just through underwriting TVL to protocol fees/revenue and applying insane TVL growth values. I believe that with Apollo joining as a governance party, we'll eventually see the fee switch flipping on to accrue value to the token. But to be honest, I can't say for sure this'll happen. I just hope the cofounders will follow the path paved by Hyperliquid and help turn the tide of a market swamped by bloated high FDV governance scams to tokens that have direct alignment with the success and growth of their respective protocols. This is the only way we can move forward and grow as an industry.

To summarize, my thesis is that institutional credit will continue to migrate onchain and at an increasing rate. Morpho seems uniquely positioned to benefit from this, serving as the AWS of this impending migration. The data supports this thesis. TVL started 2025 at $3.2B, hit an ATH of $8.6B, and is currently at $6B. 145% year-over-year growth. Apollo, Coinbase, Bitwise are already building and integrating with the stack. The main risk here is the unlock overhang and the lack of current fee capture. While governance over the credit infrastructure is valuable by itself, the true flywheel only materializes if there is a fee switch turned on, where Morpho is able to direct protocol fees to token purchases that either get burned or held in a hyperliquid-esque "assistance fund."